Off the Chain — October 2024⚙🚛📦

Since today’s news cycle is as exciting as watching paint dry… here’s your monthly dose of Supply Chain updates. Perfect reading material while you wait in line at the polls!

Connect with us: Mike McClure, Caitlin Vorlicek, Dorothy Shapiro, Mike Crowe

Off the Road✈

Our team was all Over The Road in October at the Inland Distribution conference in Chicago and TIA Technovations in Florida. Some of the key transportation technology themes we took away include:

Data → Democratization: This was a hot topic at Inland Distribution, with technology vendors helping democratize the brokerage industry by providing access to actionable, high-quality data that enables better pricing, load matching, and visibility. This doesn’t mean broker relationships won’t matter in the future – in fact, when the playing field is leveled, service becomes increasingly commoditized, and relationships will matter more than ever.

Automation (with and without humans): At TIA’s Technovator showcase, the biggest theme was automation, and the biggest question was “where does the human fit in?” Some vendors are taking a fully autonomous approach to tasks like appointment scheduling, leveraging increasingly high-quality available data, while others are taking a “human-in-the-loop” approach to maintain strong relationships with shippers and carriers. Regardless of approach, it is clear that these solutions allow brokerages to do more with less, resulting in further resilience of the small and mid-sized brokerage.

Consolidation or not?: Amidst a challenging rate environment and overall freight recession, we’ve seen brokers and carriers shutter doors or get acquired. We heard debate around whether consolidation will continue into the future, leaving the fragmented long-tale of brokerages behind. Our Team’s perspective is that consolidation is normal in a down-market, but the growth and sophistication of technology in the sector will only support the small and mid-sized broker, resulting in ongoing competition and fragmentation.

Off the Press📰

Port strike ends (for now…): On October 3rd, the ILA and USMX reached an agreement to raise wages 62% over the next 6 years that ended the largest work stoppage of its kind in decades — at least for now. The two organizations issued a joint statement last week that they will reopen discussions after the Presidential election to hopefully resolve all outstanding issues, most of which surround the use of automation in ports, and avoid a repeat interruption. The US is behind other major European and Asian ports in its use of automation, and we’ll be watching to see whether these negotiations enable us to catch up.

Hold the onions, please!: Several major fast food chains, including McDonald’s, Taco Bell, and KFC, all removed fresh onions from their offerings in certain regions after an E Coli outbreak was traced back to McDonald’s Quarter Pounders. McDonald's demonstrated impressive tracing capabilities in response to the outbreak, swiftly pinpointing the Taylor Farms Colorado Springs facility as the source of contaminated onions. This agility suggests that McDonald’s may be ahead of many peers as the industry braces for the upcoming FSMA regulations in 2026 (see more on this re: Veralto/TraceGains below).

Keeping solar at home: By signing the Advanced Manufacturing Production Tax Credit, the Treasury formed incentives for manufacturers of solar cells, modules, inverters, and more across the solar supply chain. The provisions, which are intended to make solar investment more accessible and ultimately boost domestic production, are another example of onshoring that will theoretically foster more resilient and sustainable supply chains.

Off the Street💰

Three big announcements this month signal continued interest in supply chain from industry veterans and outsiders alike:

One Newsworthy Launch: Dave Clark, former Amazon and Flexport exec, announced his new venture, Auger, with a splashy $100m Seed funding round led by Oak HC/FT. While vague on specifics, Clark describes Auger as a system that “...will integrate data from multiple sources and use advanced AI and machine learning to generate automated, dynamic insights in real time…The platform will offer a single pane of glass across planning, forecasting, and financing.” We applaud Oak HC/FT and Dave’s big swing at tackling a meaty issue, and we’ll be curious to find out whether supply chain data is abundant and available enough to deliver on a somewhat clichéd “single pane of glass” mission. We’d also be remiss not to call out Sageview portfolio company Impact Analytics, which is delivering on similar promises and counts top brands like Steve Madden, Ralph Lauren, Victoria Secret, Big Lots!, and Saks Off Fifth as customers with its retail-focused, AI-powered planning suite.

And Two Big Acquisitions: Veralto, which owns software brands innovating in water and product quality, added TraceGains to its portfolio in a $350m acquisition. History may be a nice predictor of success for Veralto’s newest brand: we saw the rapid adoption of traceability solutions in the pharma sector as a direct response to the FDA’s DSCSA regulation; with a FSMA deadline looming in January 2026 for traceability compliance in the food & beverage industry, TraceGains is poised for similar growth. Veralto specifically called out its complementary asset, Esko, focused on digitizing packaging operations, a highly underserved category for most consumer companies that Sageview portfolio company Specright is also addressing.

And Sage, a leading Office of the CFO platform, is dipping its toe into supply chain with its acquisition of Anvyl, a visibility solution for SMBs focused on purchase order to warehouse operations. By taking this integration in-house, Sage is extending its capabilities and offering a more robust suite to compete with ERPs like Netsuite and (more upmarket) SAP and Oracle.

Off the Charts📈

Chart: Public Company Multiples1:

Our team tracks eight publicly traded supply chain technology companies: WiseTech, Samsara, Trimble, Manhattan, Descartes, SPS Commerce, Kinaxis, and E2open. Mega platforms like SAP, Oracle, and Microsoft are excluded given their mix of revenue beyond supply chain.

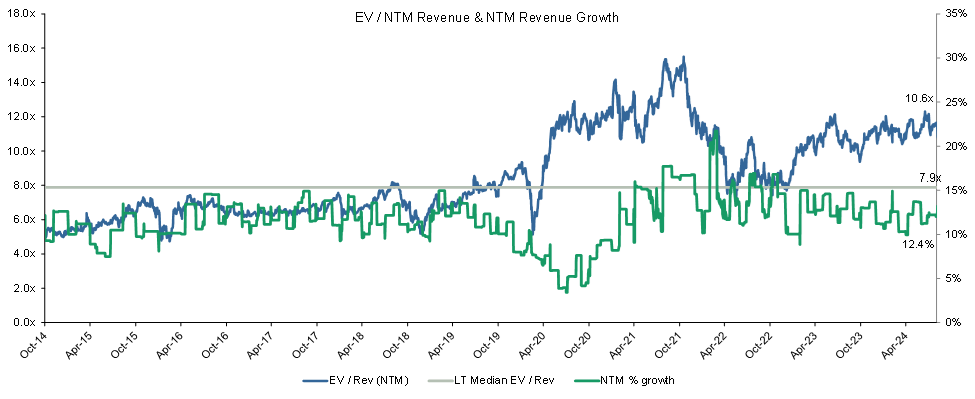

Chart: 10-Year Trading Multiples – EV / NTM Revenue & Revenue Growth:

Revenue multiples are generally correlated with NTM revenue growth, with an inverse trend post-COVID.

Current median NTM revenue multiple: 10.6x

Current median NTM revenue growth: 12.4%

10-year median NTM revenue multiple: 7.9x

Chart: 10-Year Trading Multiples – EV / NTM Revenue2:

Supply chain technology companies today are trading at a premium relative to the broader SaaS universe.

Current median Supply Chain NTM revenue multiple: 10.6x

Current median SaaS NTM revenue multiple: 4.3x

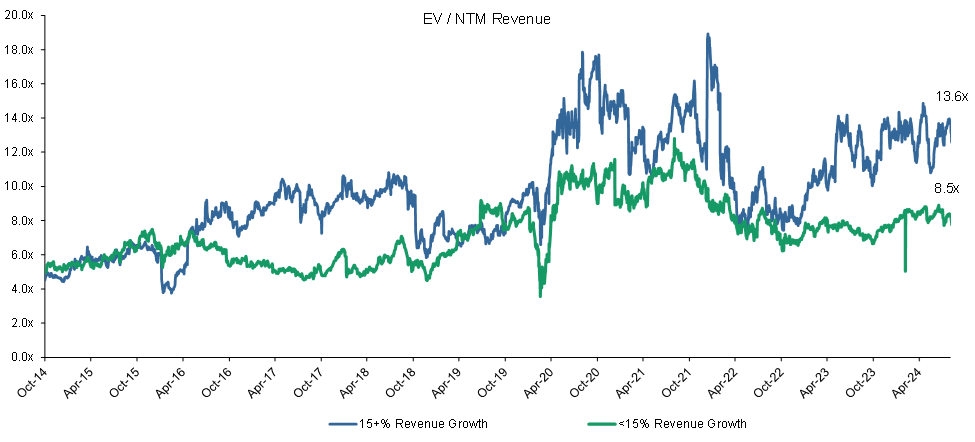

Chart: 10-Year Trading Multiples – Companies Growing +/-15%3:

There is a growing bifurcation of value for companies growing +/- 15%.

Current high growth median NTM revenue multiple: 13.6x

Current low growth median NTM revenue multiple: 8.5x

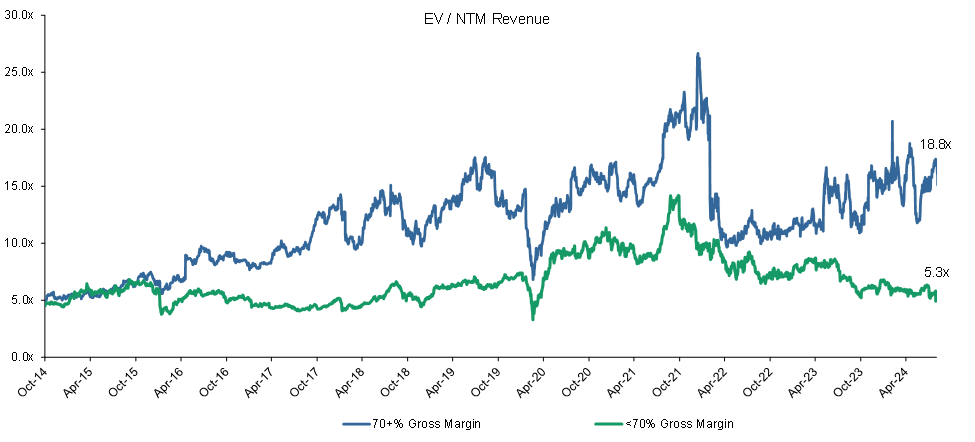

Chart: 10-Year Trading Multiples – Companies with +/-70% Gross Margin4:

Companies with SaaS-like gross margins (70%+) trade at a significant premium to companies with <70% gross margins.

Current high margin median NTM revenue multiple: 18.8x

Current low margin median NTM revenue multiple: 5.3x