Off the Chain — May 2026⚙🚛📦

Our team's supply chain takeaways from attending AI conferences and a look at the shifting tectonic plates of eCommerce fulfillment...

Connect with us: Caitlin Vorlicek, Raaga Kannan, Dorothy Shapiro, Oliver Wang, Mike Crowe

Off the Road✈️

This month we took a brief detour from the supply chain circuit to go deeper on AI, visiting Stripe Sessions in San Francisco and FirstHand VC’s AI Agent Conference in NYC. Neither was explicitly supply chain, but both left us with plenty to chew on.

Unsurprisingly, much of the Agent Conference was focused on how agents affect the size and shape of the workforce. The consensus was that the only constant will be transformation: in the words of one panelist, “be prepared for your org structure to change 15 times in the next two years.” Another leader argued that part of that reshaping will be the shift from human in the loop to “human around the loop,” meaning that human employees should not be involved in agent-delegated tasks so long as the tech makes it as easy for them to interact and communicate with the agent as they would with a coworker. It’ll be especially interesting to see whether and when this hypothesis holds true in an industry with as much exception management (and as much tech laggardry) as logistics and supply chain.

Meanwhile, Stripe Session’s data revealed that 75% of companies deploying AI aren’t seeing meaningful ROI, not because the tech isn’t working, but because they’re optimizing within functional silos instead of rethinking the workflow. ROI was also a key topic at the Agent Conference, where leaders argued that the problem is organizations adopting agentic solutions and then worrying about assessing the impact, when they should be defining success criteria upfront. The most agreed-upon success criteria was “cost per successful outcome.” The supply chain twist is that much of the lowest hanging fruit for agents to take over (chasing down documents, cutting down on carrier back-and-forth, etc.) are not always tracked as discrete metrics, making it more complicated to define the baseline.

Off the Press📰

Amazon Opens the Gates: Amazon launched Amazon Supply Chain Services (“ASCS”), opening its network (80k+ trailers, 24k intermodal containers, 100 aircraft, and parcel delivery) to other shippers, with P&G, 3M, and Land's End named as early adopters. There are many supply chain participants getting caught in the cross-hairs, from Amazon’s most direct rivals UPS and FedEx to large, enterprise, contract logistics providers. We’re also keeping an eye on tech-forward eCommerce fulfillment providers like Stord, Flexport, and ShipBob (at least Stord is still doubling down, see below). While these players explicitly leaned into technology to provide Amazon-like quality and speed, they now face direct competition from the giant itself. We’ll be watching to see whether these players can leverage AI to compete with Amazon’s scale, or if, like we’ve seen in other modes, technology is better provided by third parties.

Capacity Clears the Road: In January, we called for a “slow climb” out of the freight recession, conditional on excess capacity being shed, pointing to STG Logistics’ bankruptcy as an early signal. We were at least partially right. The ATA For-Hire Truck Tonnage Index hit 117.0 in March, up 3% YoY, the largest annual gain since October 2022. ATA Chief Economist Bob Costello called Q1 the best combined performance since Q3 2017 and, importantly, characterized this as a “supply side recovery.” That means carriers have pricing power for the first time in years, while brokers’ margins could be at risk. And with DAT week and Memorial Day Weekend in Q2, we expect to see a similar trend continue.

Off the Street💰

5/12 & 5/21: Coupa continued its acquisition spree with Rossum, an intelligent document processing platform for AP and invoicing, and Tonkean, an agentic intake and orchestration platform. Together, the acquisitions address longstanding gaps in Coupa’s source-to-pay promise, enabling customers to automatically route requests (Tonkean), execute transactions (Coupa’s core), and extract invoice data (Rossum) without manual handoffs or data entry. In January, we called 2026 the “Orchestration Era” and predicted that modular, best-of-breed stacks would challenge monolithic S2P platforms. Following the recent wave of consolidation, however, we’re asking whether vendor neutrality will continue to pull customers toward independent orchestration players like Omnea and Oro Labs, or whether the pendulum will swing back toward integrated S2P suites.

5/26: Stord raised a $250m Series F at a $3b valuation, double last year’s Series E, with backing from Strike Capital, Kleiner Perkins, and others. Alongside the raise, the company launched Stord Labs, a 10,000 square-foot R&D facility to test AI, robotics, and automation against real orders before deploying them across its nearly 100 fulfillment locations. The bet of vertically integrating the network, software, and data layer is potentially enabling a business model evolution for Stord, with software bookings (the “Consumer Experience Suite”) reportedly tripling in 2025. With the ASCS launch (see above) in tandem with this raise, we’ll be curious to see if Stord can differentiate enough from the pack to grow its valuation from here.

5/26: Global-e's $350m acquisition of Passport has first and second-order benefits worth highlighting. As has been well covered, the acquisition adds cross-border logistics depth and a non-MoR motion that expands Global-e's TAM. But the combination also supports two themes we've been watching: first, platforms that own both the workflow and the data underneath (like Passport’s carrier routing, delivery performance, and customs clears data across 220+ markets) build moats that AI can't commoditize. And second, as the parcel market bifurcates as shippers prioritize both cost savings and speed (see Amazon above, again), the winners will be those who can route intelligently by urgency, geography, and customer value. Interestingly, we think the price — $350m upfront for $100m of high-growth, EBITDA-neutral revenue — is disciplined. Kudos to Global-e for a smart buy on many fronts… the sign of a well-oiled M&A machine!

5/28: Autodesk agreed to acquire MaintainX, a modern maintenance and operations platform, in an all-cash transaction valued at approximately $3.6b. Autodesk has long owned the “design” and “make” phases of the asset lifecycle, and MaintainX is its bet on the “operate” leg. Where Autodesk’s tools document how industrial assets are designed and built, MaintainX captures how they perform in the real world, logging asset condition, maintenance history, failure patterns, and work orders from the shop floor. Together, these datasets create a more complete view of the asset lifecycle and a stronger foundation for AI that can anticipate failures before they occur rather than react after the fact.

Off the Charts📈

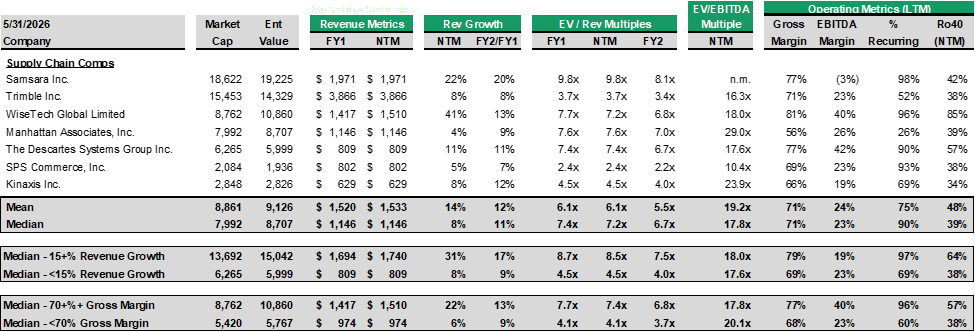

Chart: Public Company Multiples1:

Our team tracks seven publicly traded supply chain technology companies: WiseTech, Samsara, Trimble, Manhattan, Descartes, SPS Commerce, and Kinaxis. Mega platforms like SAP, Oracle, and Microsoft are excluded given their mix of revenue beyond supply chain.

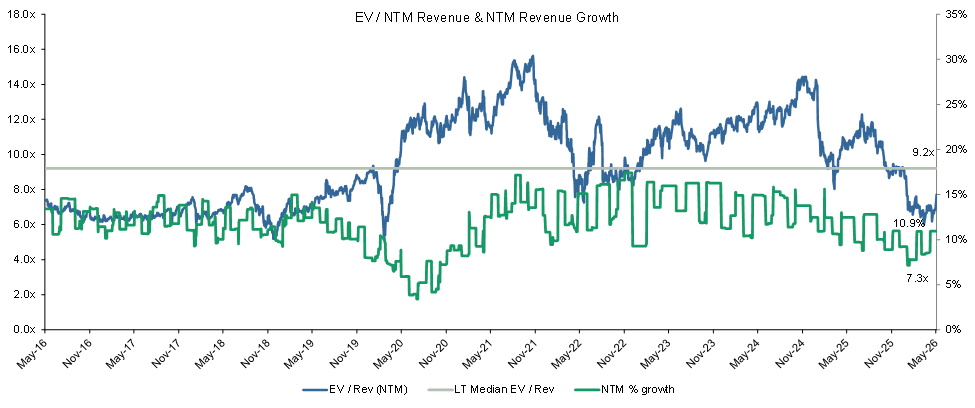

Chart: 10-Year Trading Multiples – EV / NTM Revenue & Revenue Growth:

Revenue multiples are generally correlated with NTM revenue growth, with an inverse trend post-COVID.

Current median NTM revenue multiple: 7.3x

Current median NTM revenue growth: 10.9%

10-year median NTM revenue multiple: 9.2x

Chart: 10-Year Trading Multiples – EV / NTM Revenue2:

Supply chain technology companies today are trading at a premium relative to the broader SaaS universe.

Current median Supply Chain NTM revenue multiple: 7.3x

Current median SaaS NTM revenue multiple: 2.8x

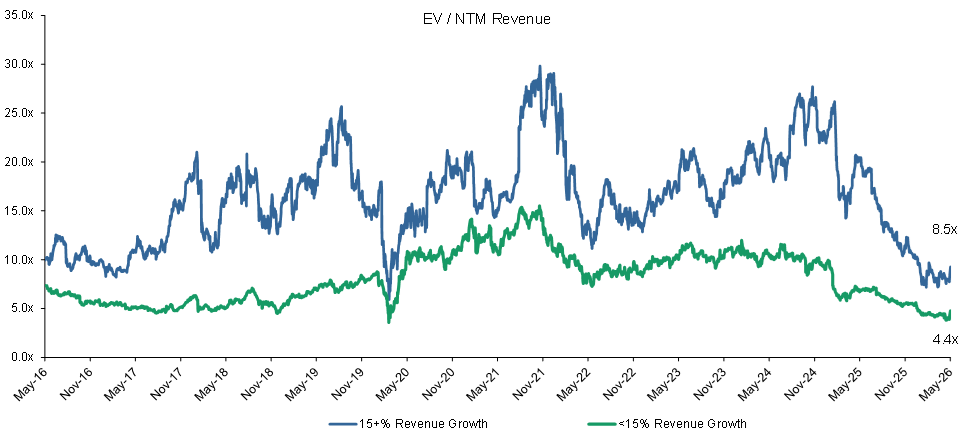

Chart: 10-Year Trading Multiples – Companies Growing +/-15%3:

There is a growing bifurcation of value for companies growing +/- 15%.

Current high growth median NTM revenue multiple: 8.5x

Current low growth median NTM revenue multiple: 4.4x

Chart: 10-Year Trading Multiples – Companies with +/-70% Gross Margin4:

Companies with SaaS-like gross margins (70%+) trade at a significant premium to companies with <70% gross margins.

Current high margin median NTM revenue multiple: 7.4x

Current low margin median NTM revenue multiple: 4.1x